- 01Visionflex said NSW Health awarded it an approximately A$0.8 million hardware supply contract for the statewide RPM Digital Uplift initiative.

- 02The order covers 127 General Examination Cameras and 162 Video Examination Camera Glass Kits for use across multiple NSW hospitals and health service organisations.

- 03Investors are likely to watch June 2026 delivery, revenue and cash collection timing, and whether the contract supports broader recurring revenue conversion amid funding and execution risks.

Visionflex Group (ASX:VFX) said NSW Health has awarded it an approximately A$0.8 million contract to supply remote patient monitoring hardware for a statewide digital uplift program. The filing marks a straightforward commercial update, with the company selected through an RFQ process for the statewide RPM Digital Uplift initiative.

The order is tied to remote patient monitoring use cases supporting Hospital in the Home and Virtual Hospital programs, according to the company. In practical terms, that means Visionflex is supplying connected clinical hardware used to support virtual care workflows rather than announcing a software-only deal or a broad memorandum of understanding.

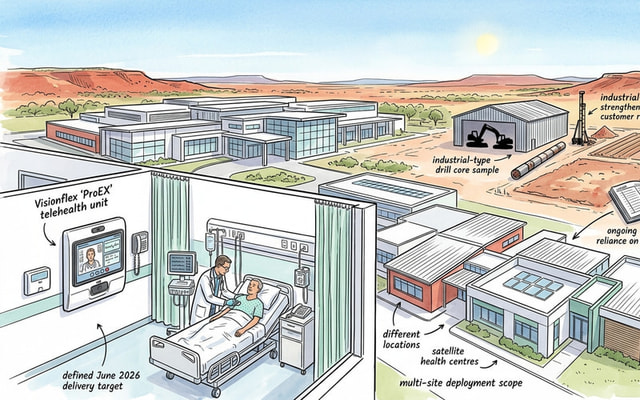

The immediate significance is that the contract gives Visionflex a defined public-sector order with a named customer, a stated program and a set delivery window. The filing also points to deployment across multiple NSW hospitals and health service organisations, which broadens the reference value of the contract beyond a single-site installation.

At the same time, the announcement is narrow in scope. Visionflex did not disclose margin, payment milestones, or whether any recurring software, maintenance or support revenue is attached to the hardware supply award. On the information released, the clearest read-through is to near-term hardware revenue visibility rather than long-duration recurring income.

NSW Program and Company Context

The project in question is NSW Health’s statewide RPM Digital Uplift initiative, where RPM refers to remote patient monitoring. Visionflex said the hardware will support care delivery in Hospital in the Home and Virtual Hospital settings, both of which sit within broader health system efforts to manage more care outside traditional ward environments.

Visionflex’s role in that setting comes from its broader virtual-care model. In its FY25 annual report, the company described itself as a health-tech provider combining proprietary software, proprietary hardware and integrated third-party medical devices to support remote diagnostics and patient care. Key products and assets named in that report included the Vision software suite, ProEX, VisionHome, and the company’s proprietary telehealth hardware.

That backdrop matters because Visionflex has been trying to reduce reliance on uneven, one-off hardware orders and lift the share of recurring software and support revenue. In FY25, total revenue fell to A$4.7 million, which the annual report attributed mainly to the absence of a large one-off hardware deployment seen in the prior year. Even so, annual recurring revenue rose 49% to A$1.9 million, while SaaS revenue increased 101% to A$1.4 million.

So while today’s NSW Health order is a hardware contract, it sits inside a business that has been telling the market its strategic priority is a higher recurring-revenue mix. That creates a two-part lens for reading the announcement: the contract adds concrete hardware work, but investors will also be looking for evidence over time that enterprise deployments lead to broader software utilisation and more predictable receipts.

Scope, Spend and Timing

Visionflex disclosed a clearly defined hardware bill of materials. The company said it is to supply 127 General Examination Cameras (GEIS) and 162 Video Examination Camera Glass Kits.

The order value is approximately A$0.8 million, and hardware delivery is expected to be completed in June 2026, according to the filing. Visionflex also said the contract terms are standard and customary for similar supply contracts.

What changed today is not a revision to prior formal guidance, but the addition of a specific order against a backdrop where previous filings had pointed to timing risk in enterprise contract execution. In H1 FY26, Visionflex said revenue was affected by the timing of enterprise contract execution and hardware delivery. That makes this NSW Health award notable because it moves from general pipeline and deployment commentary to a named, quantified order.

Still, the filing leaves several operating details open. There is no breakdown of payment timing, no disclosure of manufacturing economics and no statement on whether this hardware award includes follow-on software subscriptions or services. Given Visionflex’s revenue mix has historically been influenced by the timing of large deployments, those details may matter when the market later assesses how much of the contract converts into recognised revenue and cash receipts within the expected period.

What to Watch Next

The first milestone is the most obvious one: completion of hardware delivery by June 2026. Because the contract has a defined unit scope and a short delivery window, execution risk now centres on procurement, manufacturing, logistics and rollout across the relevant hospital and health service sites.

The second issue is cash conversion. Visionflex’s recent disclosures show why that remains important. In the March 2026 quarter, the company reported A$507,000 in cash at quarter end, A$850,000 of unused financing facilities and an estimated 2.01 quarters of funding available, while recording negative operating cash flow of A$676,000 for the quarter.

Funding support remains part of the company’s operating backdrop. The FY25 annual report said Visionflex had A$1.9 million cash at 30 June 2025 and A$3.4 million in cash and funding access including unused finance facilities at that date, but it also stated the company was not profitable and did not expect profitability until further commercialisation supported ongoing operations. The company’s debt profile at that point was dominated by convertible notes provided by John Plummer and Adcock Private Equity Pty Ltd, with available undrawn facility support referenced in the report.

More broadly, the annual report and quarterly filings flag ongoing risks around commercialisation, key customer contracts, supply chain dependence and regulatory compliance linked to supplying medical devices. Against that backdrop, the NSW Health order is useful as a tangible public-sector reference point, but the next read-through is likely to come from evidence of delivery, revenue recognition and collection timing rather than the contract announcement alone.

Public-sector Proof, Execution Still Matters

The NSW Health award gives Visionflex a concrete A$0.8 million public-sector hardware contract with a defined June 2026 delivery target and multi-site deployment scope. It strengthens the company’s customer reference base, but the filing leaves open questions around margin, recurring revenue attachment and cash conversion, all of which sit against a backdrop of ongoing cash burn and reliance on funding facilities.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.